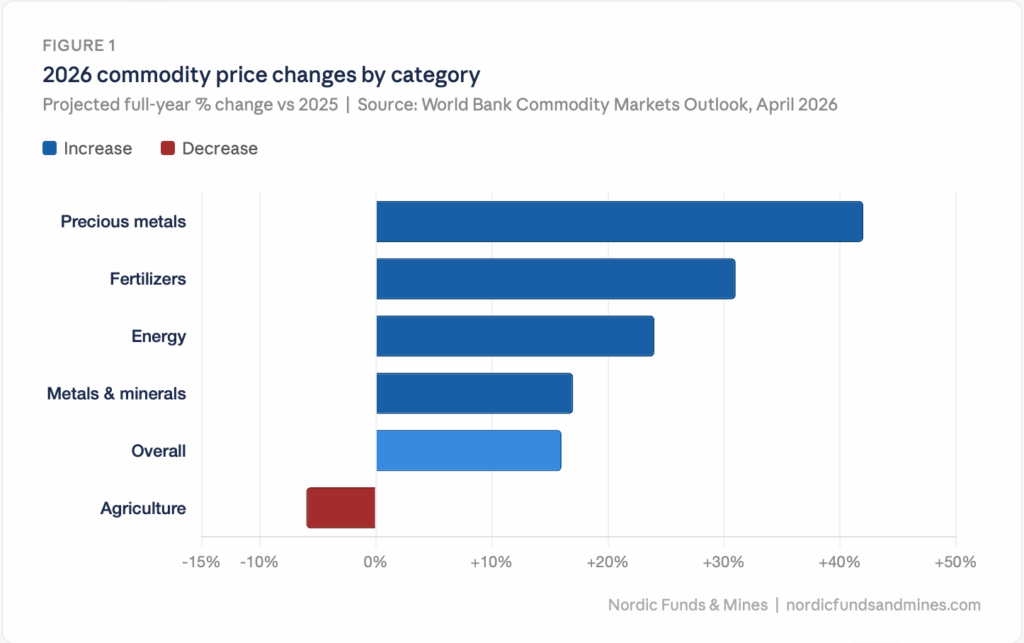

Something shifted in early 2026 that markets had not fully priced. Global commodity prices are now tracking a 16 percent annual increase, the first since 2022, and the figure dramatically understates the dispersion underneath it. Precious metals are heading toward a 42 percent gain and new record highs. Energy and fertilizers are up 24 and 31 percent respectively. Metals and minerals have added 17 percent. The only category moving against the tide is agriculture, down an estimated 6 percent as the cocoa and coffee supply crunches that defined 2024 and 2025 finally unwind.

This is not a demand-driven cycle. The mechanism is supply disruption and the geopolitical repricing of risk. The war in the Middle East, the vulnerability of the Strait of Hormuz, and the structural exposure of critical mineral refining to a small number of jurisdictions have all been forced into the open simultaneously. For investors and companies operating in the resource sector, the question is no longer whether this environment is significant. It is whether their positioning reflects it.

Figure 1: Projected full-year % change, 2026 vs 2025, by commodity category.

Energy: The Shock and Its Unwind

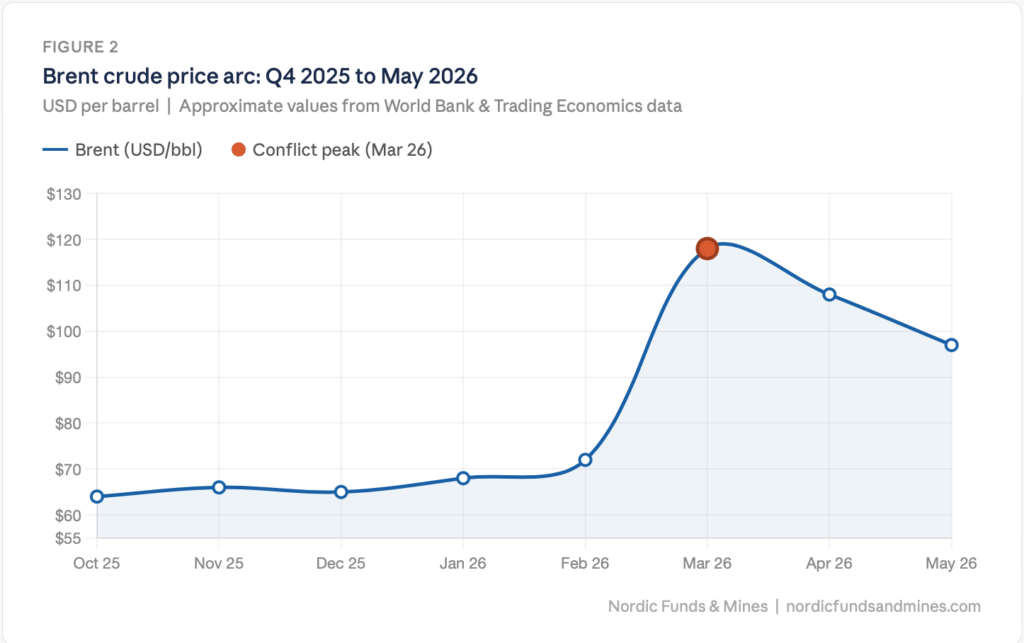

The energy story of 2026 has two chapters. Chapter one was brutal. Brent crude rose 20 percent in the first two months of the year before the conflict escalated in mid-March, at which point severe disruptions to oil shipments through the Strait of Hormuz and direct attacks on regional energy infrastructure sent Brent above $100 per barrel for the first time since 2022. By the end of March it had reached $118, the largest single-month increase on record. The Asian LNG benchmark surged 94 percent over the course of March. European natural gas prices rose 59 percent in the same period.

Chapter two is an incomplete ceasefire. As of late May, Brent has pulled back to approximately $97 and WTI is near $94, as US-Iran negotiations have progressed toward an initial agreement. Secretary of State Rubio indicated talks may take several more days. The US Navy has resumed escorting tankers through the Strait of Hormuz. Iran’s Revolutionary Guard fired on an F-35 that entered Iranian airspace. Neither side has fully stood down.

The World Bank now projects Brent to average $86 per barrel for full-year 2026 and $70 in 2027, assuming the most acute phase of disruptions ends within Q2. Global oil inventories are tightening at record speed as strategic reserves and commercial stockpiles are drawn down to offset lost supply. Barclays is maintaining its 2026 average forecast at $100 per barrel. The downside scenario requires a clean ceasefire, a fully reopened Hormuz, and a faster-than-expected recovery in Middle East export capacity. None of those is certain.

Figure 2: Brent crude price movement from Q4 2025 through late May 2026, with March 2026 Hormuz disruption peak annotated.

Gold and Precious Metals: Consolidating, Not Collapsing

Gold is trading near $4,500 per ounce as of late May, approximately 15 percent below its conflict-driven peak. The pullback reflects a single thesis: an energy-driven inflation shock reinforced expectations that central banks would hold rates higher for longer, pressuring non-yielding assets. Federal Reserve Governor Waller recently signaled the bank no longer believes it should retain an easing bias in its policy statement.

The longer-term picture remains structurally constructive. In 2025, gold climbed approximately 65 percent and silver approximately 144 percent, the largest annual gains for both metals in over four decades. Precious metals are still projected to gain 42 percent for full-year 2026 and reach record highs. The recent oil price decline has begun easing the inflation concern that drove the pullback, and US-Iran agreement progress has reduced safe-haven urgency without eliminating it.

For junior and intermediate gold miners, the financing environment remains the most supportive in years. Gold-focused companies continue to raise more capital than any other metal category, including copper. Management teams with credible assets and institutional-quality investor relations are finding audiences that were largely absent three years ago.

Base Metals and Critical Minerals: The Structural Story

Copper’s move higher in 2026 is being driven by a convergence of factors that cannot be resolved quickly: AI infrastructure demand pulling forward years of anticipated consumption, tightening supply chains linked to the Gulf disruption, and a structural deficit that J.P. Morgan Global Research forecasts will be the largest in 22 years. Aluminum has been the most severely affected base metal, given the Middle East’s direct role in global supply, with prices projected to rise approximately 22 percent for the full year.

The most important near-term policy catalyst in this space: the US Secretary of Commerce is required to report on the domestic copper market by June 30, 2026, determining whether to impose a universal duty of 15 percent from 2027 and 30 percent from 2028. If implemented, this would materially reprice North American and allied-jurisdiction copper assets and accelerate the shift of investment capital toward non-Chinese supply.

The concentration problem in critical minerals has not improved. The average market share of the top three refining nations across copper, lithium, nickel, cobalt, graphite, and rare earth elements rose to 86 percent in 2024, with China dominating every category except nickel. Western government urgency is real, and capital is following. The US government committed over $14.8 billion in Letters of Interest for critical minerals projects under the current administration. The EU’s planned support of approximately EUR 3 billion in 2026 is a fraction of what the first wave of strategic projects will actually require, making private capital, including Nordic family offices and institutional investors, the essential bridge.

The Fennoscandian Opportunity

The Fennoscandian Shield, the ancient geological formation stretching across Norway, Sweden, and Finland, is receiving accelerating attention as the European Critical Raw Materials Act creates policy urgency for domestic supply. Sweden alone holds documented resources across at least nine EU-designated critical raw materials. The market is already responding: Turnstone Resources rebranded in March 2026 from a potash company into a Scandinavian copper, gold, and rare earth explorer, explicitly targeting the European strategic metals thesis. Junior exploration companies, often backed by North American and Australian capital, are increasingly selecting Nordic jurisdictions for their geological endowment, regulatory stability, and alignment with European supply chain policy.

What This Means for Nordic Investors

Norway’s sovereign wealth fund reported a 0.6 percent investment loss in Q1 2026 as global equity markets fell in response to the conflict. The fund’s annual white paper, published in March, noted directly that the war has pushed oil prices higher while reducing the fund’s equity portfolio value, a reminder that Norway’s dual exposure to energy revenues and global capital markets produces non-linear outcomes in shock scenarios.

For Nordic institutional investors more broadly, the structural positioning question is sharpening. Critical minerals are no longer a thematic overlay on an energy transition narrative. They are increasingly treated as a core allocation aligned with electrification mandates, European industrial security policy, and the kind of long-duration supply chain arguments that Nordic pension funds and family offices understand well. The question is no longer whether to have exposure. It is through what instrument, at what stage, and in what jurisdictions.

Public markets remain the most accessible and liquid entry point. Junior mining companies listed on TSXV, CSE, and equivalent exchanges offer early-stage exposure with defined catalysts, published technical reports under NI 43-101 or equivalent standards, and management teams increasingly structured for institutional-quality engagement. The challenge is identification, diligence, and access. That is precisely the problem Nordic Funds & Mines was built to solve.

Written by: Moneer Barazi, Head Analyst at Nordic Funds and Mines